What is the 50 30 20 rule money saving expert?

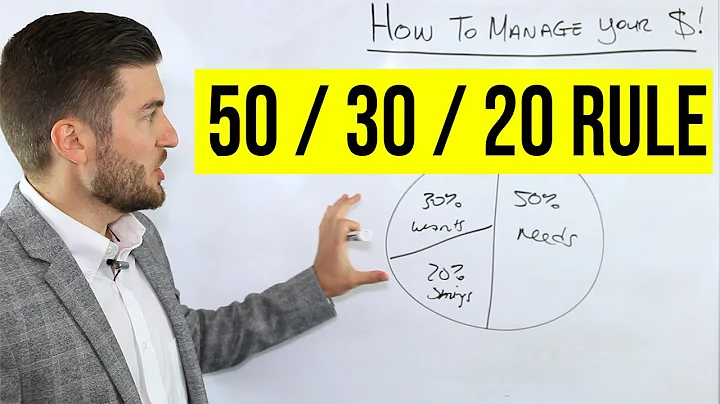

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals. Let's take a closer look at each category.

The 50/30/20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

The 50/30/20 rule can be a good budgeting method for some, but it may not work for your unique monthly expenses. Depending on your income and where you live, earmarking 50% of your income for your needs may not be enough.

To best use the 50/30/20 rule, balance your current income and expenses with your short- and long-term goals. Let's say you earn $2,500 per month after taxes. You'll aim to spend no more than $1,250 on necessities and $750 on wants, leaving $500 for savings and debt payments.

Our 50/30/20 calculator divides your take-home income into suggested spending in three categories: 50% of net pay for needs, 30% for wants and 20% for savings and debt repayment. Find out how this budgeting approach applies to your money.

Figure out what's realistic for you

The 20% rule is a good general guide, but it isn't the right fit for everyone. Some people can save above that rate, while others merely struggle to make ends meet. “Some people pay their rent and they have nothing left.

Are you approaching 30? How much money do you have saved? According to CNN Money, someone between the ages of 25 and 30, who makes around $40,000 a year, should have at least $4,000 saved.

Bottom Line. Living on $1,000 per month is a challenge. From the high costs of housing, transportation and food, plus trying to keep your bills to a minimum, it would be difficult for anyone living alone to make this work. But with some creativity, roommates and strategy, you might be able to pull it off.

The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals.

The rule says that 50% of your after-tax income must be spent on needs and obligations that you have to meet, such as rent and utilities. The remaining half should then be split between 20% savings and debt repayment and 30% to your wants and entertainment.

Is the 50 30 20 rule gross or net?

50% of your net income should go towards living expenses and essentials (Needs), 20% of your net income should go towards debt reduction and savings (Debt Reduction and Savings), and 30% of your net income should go towards discretionary spending (Wants).

Does 401(k) count as savings in a 50/30/20 budget plan? Yes, a 401(k) can count as savings in a 50/30/20 budget plan. But if 401(k) contributions are automatically deducted from your paycheck, they're not included in your take-home pay calculation.

The Takeaway

Using them, you allocate your monthly after-tax income to the three categories: 50% to “needs,” 30% to “wants,” and 20% to saving for your financial goals. Your percentages may need to be adjusted based on your personal circ*mstances and goals.

If you're looking for a ballpark figure, Taylor Kovar, certified financial planner and CEO of Kovar Wealth Management says, “By age 30, a good rule of thumb is to aim to have saved the equivalent of your annual salary. Let's say you're earning $50,000 a year. By 30, it would be beneficial to have $50,000 saved.

20% is allocated to investment and retirement accounts, such as a 401(k), IRA, or other savings accounts, which may include a sinking fund.

The 70-20-10 budget formula divides your after-tax income into three buckets: 70% for living expenses, 20% for savings and debt, and 10% for additional savings and donations. By allocating your available income into these three distinct categories, you can better manage your money on a daily basis.

The 30% Rule Is Outdated

To start, averages, by definition, do not take into account the huge variations in what individuals do. Second, the financial obligations of today are vastly different than they were when the 30% rule was created.

Saving $1,500 per month may be a good amount if it's feasible. In general, save as much as you can to reach your goals, whether that's $50 or $1,500. You could speak with a certified financial planner to help develop a plan for your finances if you aren't sure how much money to save regularly.

When your savings reaches $100,000, that's a milestone worth marking. In a world where 57% of Americans can't cover an unexpected $1,000 expense, having a six-figure savings account is commendable.

After analyzing many scenarios, we found that 75% is a good starting point to consider for your income replacement rate. This means that if you make $100,000 shortly before retirement, you can start to plan using the ballpark expectation that you'll need about $75,000 a year to live on in retirement.

Is $600000 in savings good?

With $600,000 in savings at age 50, an early retirement becomes even more feasible. Applying the 4% rule, you could withdraw $24,000 per year, or $2,000 per month. As long as you maintain moderately frugal living expenses under $24,000 per year, you should be able to leave your career by 50.

Yes, I can and do, but it depends on a person's circ*mstances. If you have a mortgage, a car payment and other bills, you may not be able to. If you live in an area where rents are high, you may not be able to. $100 a day equals $3000 a month and a lot of peoole live well on less than that.

You can retire comfortably on $3,000 a month in retirement income by choosing to retire in a place with a cost of living that matches your financial resources. Housing cost is the key factor since it's both the largest component of retiree budgets and the household cost that varies most according to geography.

Living on $2,000 per month is doable, but you won't be able to live just anywhere. This is important because at the time of writing the average Social Security benefit paid is $1,701 per month.

4) 1st Week Rule

To bring discipline in investing, personal finance experts advise you to save and invest the 20% allocated amount for savings from your income in the first week itself.